The problem

Underwriting a flip looks easy until you’re staring at a property a lender wants a number on by Friday. The pieces — comps, condition discount, rehab budget, max-allowable offer — live in three different tools, and the lender wants a single document that ties them together. Solo flippers and small wholesalers don’t have an analyst to pull it together; they have a phone and an evening.

What we built

HomeFlippy is one tool from “I found a property” to “the lender funded the deal.” Drop in an address and 20 phone photos; out comes a condition-adjusted ARV, a zip-calibrated rehab budget, a max-allowable offer, and a lender-ready PDF — with every number traced back to the comp or photo that drove it.

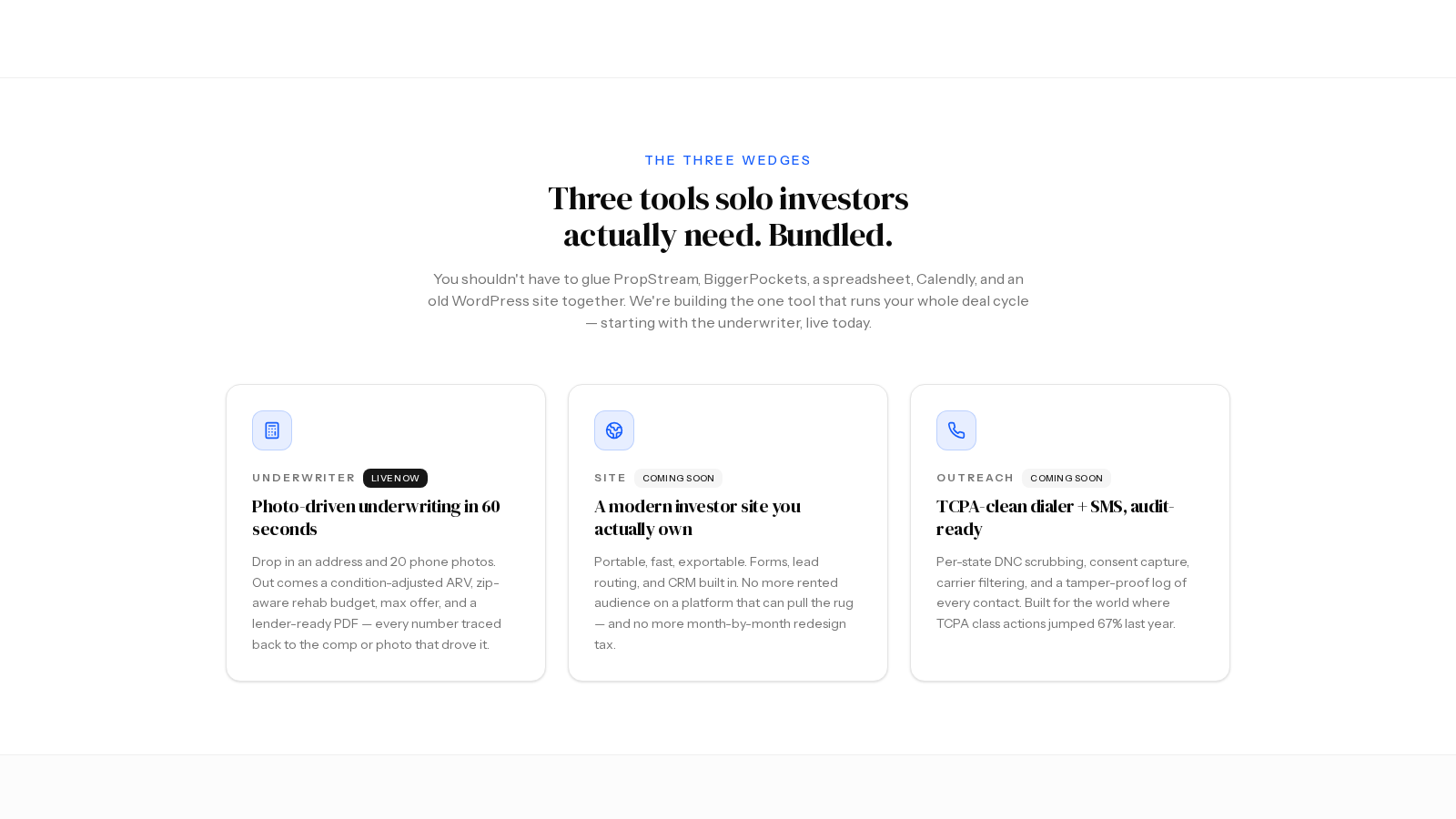

The product is three apps that belong together. The underwriter does the math from photos in about a minute. The saved-deals dashboard organizes the deals you’re working, with one-click shares to a lender. The outreach side is a TCPA-clean dialer + SMS workflow with the audit trail your compliance lawyer wants to see.

The free tier is a Zillow-URL calculator with no signup; the paid underwriter unlocks the full photo-grading + lender PDF pipeline.

How we shipped it

Owned code on owned infrastructure — Laravel + Inertia + React on the box, Postgres + Redis for state, S3 for photos, SES for email, CloudFront in front. The vision and reasoning calls go to OpenAI’s GPT-5 family for the photo grading and ARV/rehab math; everything around them is normal Laravel — queueable, testable, debuggable.

The PDF is the deliverable lenders actually read at 9pm; we wrote it for that reader, not for a marketing screenshot.

Outcome

HomeFlippy is live. Solo flippers can paste a Zillow URL and get a calculator number for free, or run the full photo-driven underwrite + lender PDF for the price of a streaming subscription. The company that owns the code owns the model, the data, and the relationship with the lenders — not a SaaS landlord.